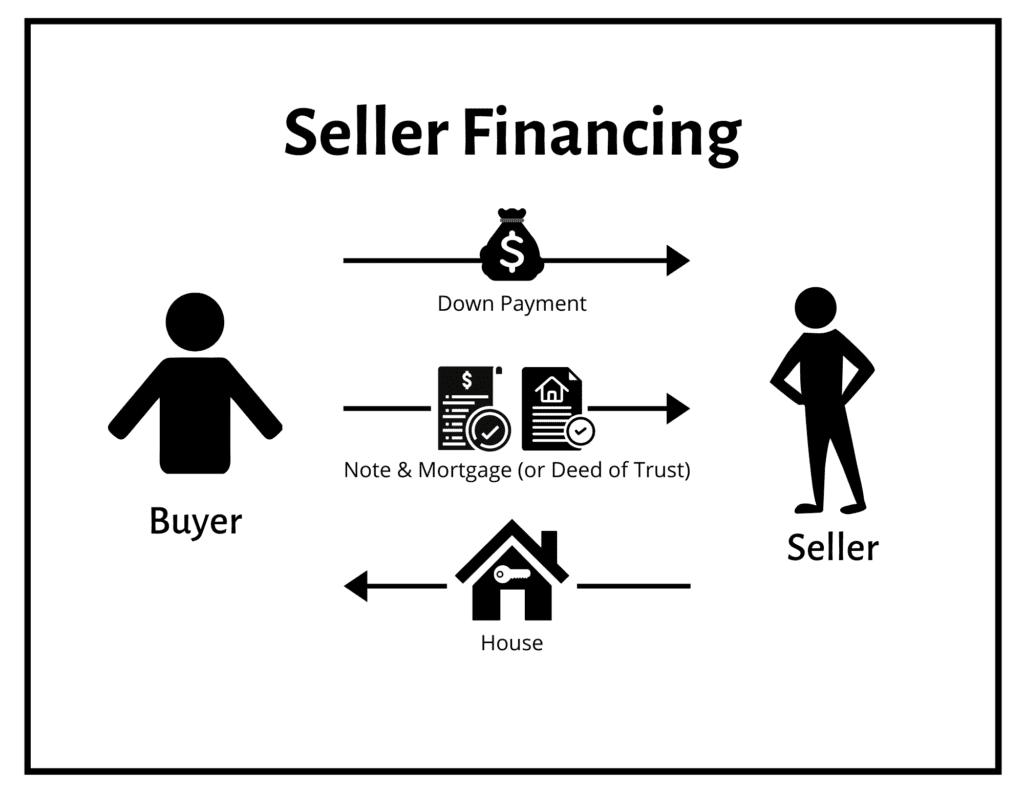

When a real estate seller allows their buyer to make payments over time, it’s known as seller financing.

This private financing can take the place of a bank loan or could be in addition to a conventional mortgage.

The payment amount, interest rate, and other terms are agreed upon between the buyer and seller. The amount financed by the seller will depend upon the down payment, and whether there are any bank loans.

Real Estate Bank Loans vs. Seller Financing

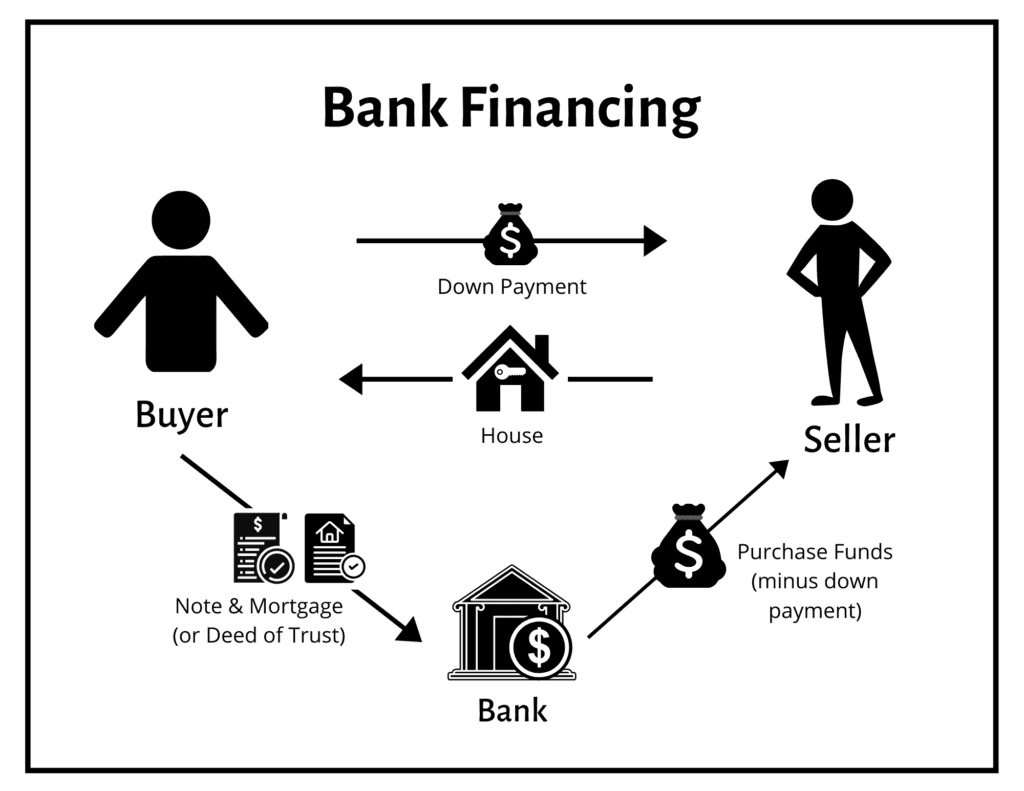

While most private real estate buyers obtain loans from a bank or other large financial institutions, it’s not the only way. With seller financing, the seller acts as the bank. They accept payments over time, and the property serves as collateral for their loan.

The buyer is making payments to the seller rather than an institutional lender. Other terms for this type of legal arrangement are “private mortgage,” “seller carry-back,” and “installment sale.”

Specific federal and state laws, such as the Dodd-Frank Act place restrictions on the number of loans someone may originate in a given year, proving the borrower’s ability to repay, and parameters like interest rates. Yet, there is still latitude regarding the terms each party may agree to. A seller may request a down payment, collect interest, and charge late fees.

The seller has the same rights as a bank. Therefore if the buyer does not make payments, the seller can file foreclosure.

Here’s an example of how it works:

- A property owner advertises his or her house for sale, either on her own or through an agent.

- A buyer makes an offer.

- The buyer and seller agree upon a sales price of $175,000 with a 10% down payment of $17,500.

- Rather than requiring the buyer to obtain a bank loan, the seller offers seller financing

- The Seller carries back a balance of $157,500 in the form of a note and mortgage or Deed of Trust.

- The promissory note spells out the terms of repayment. In this case, they agree upon 8.5% interest at $1,211.04 per month based on a 360-month amortization.

- The seller doesn’t want to wait a full 30 years for payments. The note requires payment in full, known as a balloon payment, within seven years.

- A title company or real estate attorney is used for the closing to be sure all parties are protected.

How Can I Offer Seller Financing?

Offering Seller Financing is quite simple. Many title and escrow companies have experience and can provide the necessary paperwork. But, to cover yourself further, it’s advised to consult with a local real estate attorney who will make sure you stay compliant with local, state, and federal laws. They should also ensure that your lien is enforceable should your borrower cease making payments down the road.

Last, but certainly not least, is to create a note that holds its value should you ever decide to sell all or part down the road. Attorneys and title or escrow companies are not versed in note valuations.

Fortunately, we are. Contact us before you negotiate your note terms, and we’ll be happy to help.

Other articles you may enjoy: